Expert insightsInvestingSpeculative heat removed from the housing market by the credit squeeze: Pete Wargent

Speculative heat removed from the housing market by the credit squeeze: Pete Wargent

It's well known that most market predictions are a waste of time: they usually just project more of what's been happening, and are rarely much chop at picking turning points.

With almost no housing market activity over the long Easter break, this does feel like a potential inflection point - for better or worse - and certainly it's as a good a time as any for a largely baseless opinion piece.

It's clear that the speculative heat has been well and truly removed from the housing market by the credit squeeze and a range of other factors.

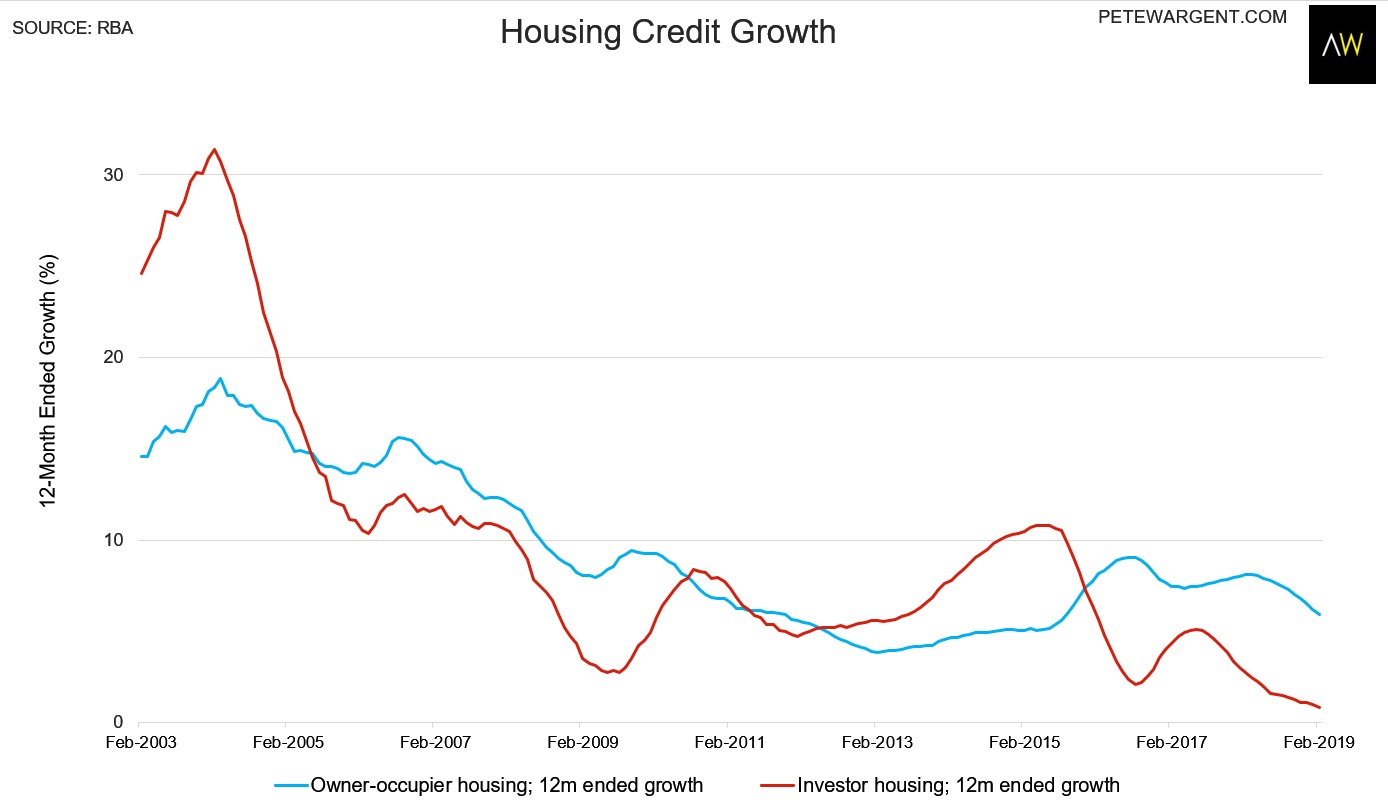

In fact, the reverse is now the case, with investor credit growth running at the lowest level in Australia's history.

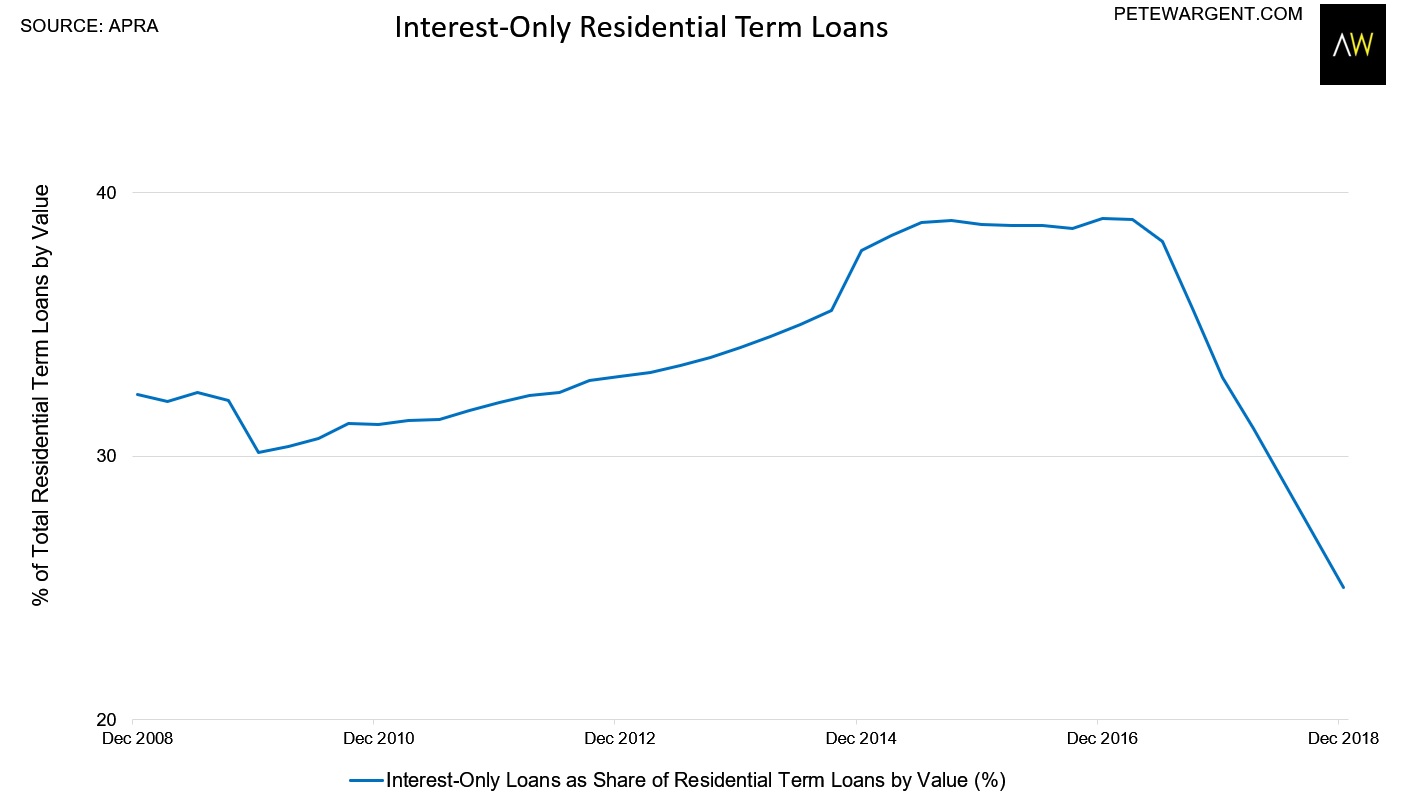

The stock of interest-only loans has been spectacularly reduced by regulatory tweaks and is also at the lowest share on record: probably down to about 21 per cent of residential loans by value by the end of this quarter, representing an epic decline from 39 per cent in early 2017.

The share of high LVR lending is also tracking at around the lowest level on recent record.

Low-doc lending, meanwhile, has been all but eliminated over the past decade.

Average paper net rental losses (aka. 'negative gearing') claimed are at the lowest level in almost a decade-and-a-half, with further declines in the post on rising yields, lower mortgage rates, and changes to allowable deductions for plant and equipment depreciation and travel.

With loans being tested for serviceability at 7¼ per cent lending metrics have, if anything, become too conservative, and borrowing capacity has in many cases been reduced by 20 to 40 per cent (or simply eliminated entirely for many portfolio investors).

Almost every way you look at it, credit has rarely been so tough to come by.

Prices cooled since early 2017

If the housing market downturn was to end here then I reckon most sober commentators and respected international observers would applaud a job well executed.

In any event, a lot of the 'bubble' talk is way overdone.

There's a lot of debt on a gross basis; but mortgage serviceability isn't particularly stretched, while there's also been an unprecedented build-up in cash and cash equivalents, mortgage buffers, and balances in offset accounts.

In Adelaide it's not all that hard to buy a house for the same price as a decade ago, which given where mortgage rates have gone must represent about a 50 per cent improvement in affordability (without backing this statement up with any hard numbers).

In Brisbane apartment prices are often seen to be lower than they were almost a dozen years ago, so affordability is now stupendously high compared to where it was.

The major house price gains since 2012 were seen in Sydney, where median prices have since declined over a period of more than two years by about 13 per cent, representing a real decline versus incomes nudging about 20 per cent from the peak (much more in parts of Western Sydney, according to a piece in the AFR this week).

It seems that most of the regulatory actions taken to cool the housing market have all but washed through, but despite the lower fixed mortgage rates on offer lately market activity is still awfully gummed up.

And there's still a non-trivial possibility that the actions taken to promote financial stability, in the end, sink it.

The economy has been stymied for some time now, with two consecutive quarters of negative GDP growth in per capita terms possibly set to be repeated for a third quarter. Consumption and retail are weak.

It's difficult to get an accurate real-time reading of housing market turnover but many experienced commentators seem to believe it's at the lowest level on record.

So, what gives?

Responsible lending: level up

A major part of the challenge for activity in the housing market is some of the breathtaking pedantry related to mortgage applications, which I've experienced a bit of, but often only mortgage brokers have a really good feel for.

There's always a chance that responsible lending morphs into a nanny state mentality, and this is now almost literally becoming so in some cases.

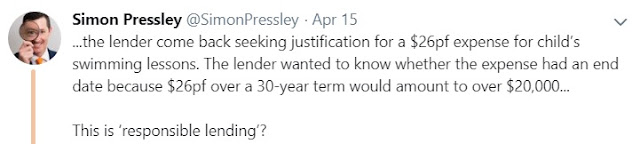

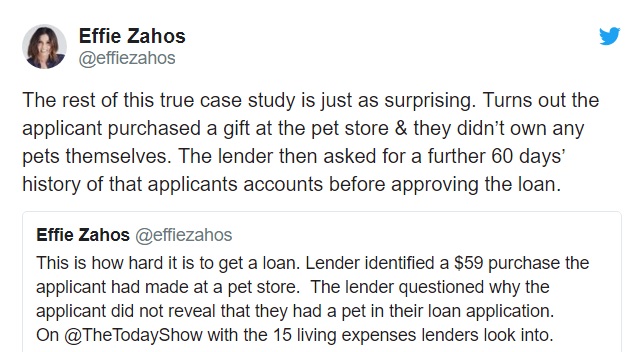

When lenders are stress-testing for scenarios incorporating up to the equivalent of a dozen or more rate hikes it defies belief that a homebuyer registering for Netflix or using Uber might be grounds for the refusal of a loan, but the banking Royal Commission brought this level of paranoia to the fore.

These sometimes amusing and apparently trivial examples are merely the tip of the iceberg in what has been at times a truly Titanic pile of administrative poppycock.

Everyone involved in mortgage lending knows that consumer behaviour and discretionary spend changes post-purchase, so all this rigmarole is largely fruitless and may now be effectively adding to FS risks rather than reducing them.

Tipping point

Lower interest rates alone don't fix this; but in truth I don't know what does.

Maybe it's the simply passage of time.

Perhaps lenders need some assurance that they aren't going to be hauled over the coals even more than has already been the case.

By the same token prospective homebuyers would doubtless like to see more certainty given the recent shifting of goalposts (with further changes to market dynamics now proposed by the Labor Party).

Whatever's the case, something needs to get mortgages flowing dependably again, or else there's a risk that the measures to shore up risks in the housing market will no longer be hailed as a success, but instead blamed for capsizing it.

Pete Wargent

Pete Wargent is the co-founder of BuyersBuyers.com.au, offering affordable homebuying assistance to all Australians, and a best-selling author and blogger.