Given the weak state of other sectors of the economy, the Retail Trade figures for the month and the June quarter took on an added significance.

In this context, especially given soft wages and slowing population growth, the June data was happily very good.

In seasonally adjusted terms retail turnover was up by 0.7 per cent for the month leading to a strong annual result to June 2015 as charted below.

State versus stateAt the state level the impact of Sydney's housing boom and to a lesser extent that of

Melbourne is evident with retail turnover rising very strongly in New South Wales and Victoria.

Perhaps more surprisingly, in turnover terms retail appears to have fired up a little elsewhere too, particularly in South Australia.

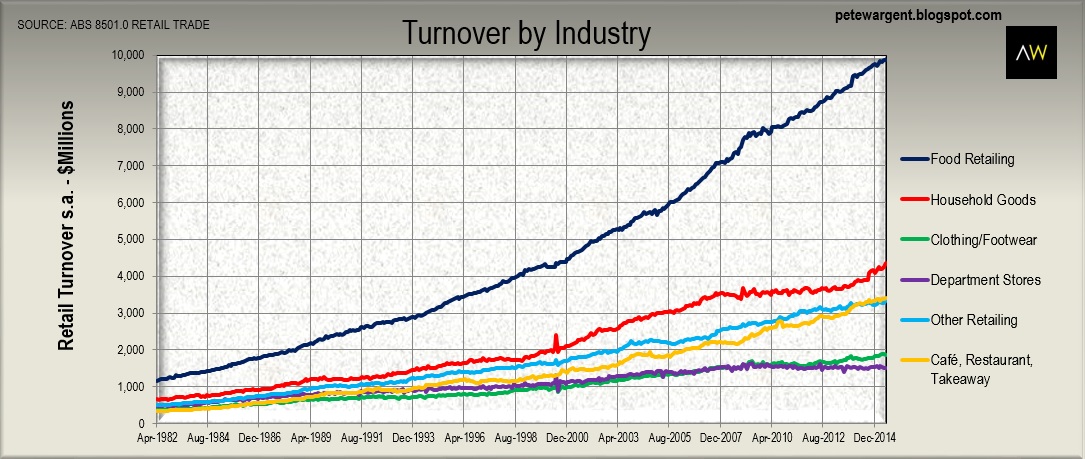

Industry groups

It has been a relatively poor time for department stores retailing, perhaps reflective of increasing demand in the online shopping space.

The big winner over the past year has been household goods with retail turnover pumped up by the housing prices and construction boom.

Cafés, restaurants and takeaway expenditure has also continued to rise relentlessly over the past year, a trend which has been ongoing over the past decade, another shift which feeds off increased apartment dwelling.

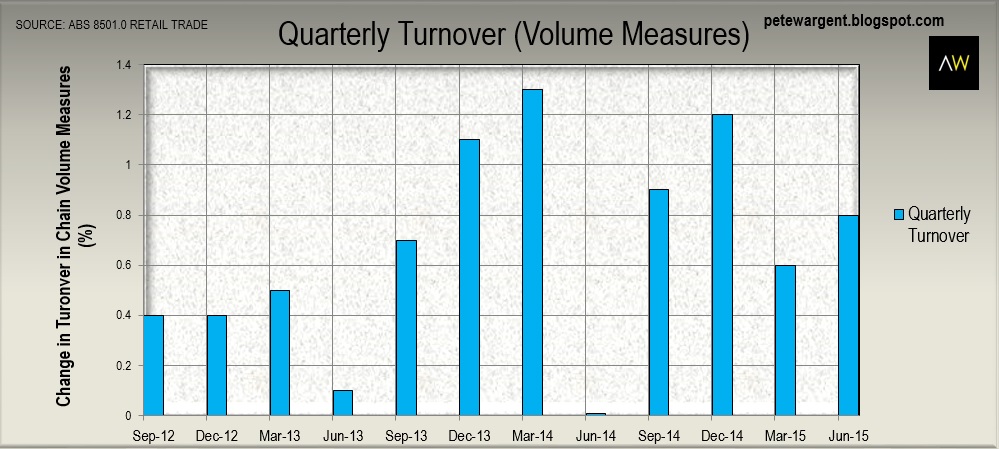

National accounts for Q2With June being the last month of the second quarter we also got the turnover figures reported in volume terms, which threw out an excellent result.

Retail volumes doubled market expectations to be up by 0.8 per cent for the quarter and 3.6 per cent for the year.

I used to do a chart here on quarterly volumes at the state level, but to be frank it's a Sunday morning and believe it or not I actually have better things to do!

Suffice to say that New South Wales (+4.6 per cent) and Victoria (+4.4 per cent) have been the retail trade linchpins over the year to June 2015.

This is a very notable result given that net exports (which have contributed significantly to GDP over the past year) will evidently not been doing so in the second quarter.

I looked at how Australia racked up a record trade deficit for the second quarter in a little more detail here.

The wrap

Overall this was a really good result for retail trade in the second quarter.

And although the retail trade data is not necessarily representative of all household consumption this suggests that GDP for the second quarter will be held up by the strong capital city economies.

Lately various surveys have hinted at gradually improving business conditions and confidence - and jobs growth has been strong over the past year at +233,600, particularly so in Sydney.

On the other hand capital expenditure surveys have pointed towards very weak business investment.

In that context, it is important that household consumption continues to produce sound results.

The other contributor to a surprisingly upbeat GDP print in the first quarter (ex-inventories) was that of new housing, with the dwelling construction boom expected to continue over the next couple of years.