Tips for deciding when you should buy property according to a property investor

I’m going to take my broker hat off for a minute and put my investor hat on because if you ask anyone working in the real estate industry they’ll usually tell you now is the best time to buy. Here are my thoughts on making the decision of when to buy property.

People commonly buy property with the following two purposes:

1. To live in as an owner-occupier

For buyers looking to purchase their first home or upgrade from their current home, the question of ‘when to buy’ is almost irrelevant. You’re not trying to time the market – you’re buying because you have a need – whether it be needing a bigger home to accommodate your growing family or simply wanting your own place to call home (rather than a rental).

The government understands that this group of buyers are the pillars holding the property fort at the moment (and will continue to do so until investor sentiment improves). That’s why the current grants are primarily focused on incentivising buyers entering the market.

2. As an investment property to accumulate wealth

The other side of the property spectrum is those who are looking to purchase property as an investment in order to accumulate wealth. This group researches the right time to buy property because they want to “time the market”.

Now I’m terrible at timing the market. So my personal approach has always been rather than trying to time when the bottom of the market is, I prefer to accumulate when I can and hold for the long-term. That to me is called investing and that’s how the Baby Boomers are able to accumulate wealth through property in the long run – whether it’s through their own home or investment property.

“But David, all the media is saying the property prices are dropping and some even say up to 10 or 20%! If we buy something now aren’t we catching a falling knife?”

Sure, no one knows what will happen to the property value and the real impact of COVID-19 may not have fully shown itself yet. So yes, prices could still continue to drop. However, you could also be up for a long wait if you’re looking at a crashing figure like 20% or 30% as predicted by some economists.

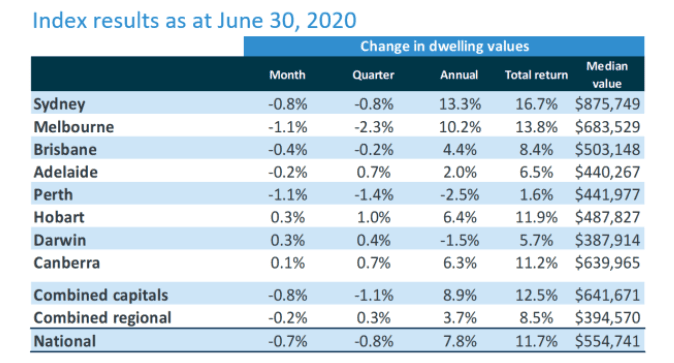

Looking at the Corelogic index published back on 30th June 2020:

Sydney and Melbourne’s dwelling value are the biggest hit so far (apart from Perth), with Sydney at a 0.8% drop for the quarter and Melbourne 2.3% drop. That’s somewhat expected due to border lockdown so no new immigrants = less demand for properties from both a rental and buyin g perspective. If you look at the annual change for both cities, the median value of these two capital cities has still shown a stellar growth of 13.3% for Sydney and 10.2% for Melbourne respectively.

The point here is property is an asset class that is not as liquid. Unlike shares it cannot be converted into cash easily – it takes weeks, if not months, to buy or sell a property. As such the price doesn’t fluctuate as much as share prices and chances are we’ll continue to see small incremental changes all the time – similar to what we have observed to-date.

With so much money printing around the world – this will typically inflate asset prices. We’re already seeing such a phenomenon in the United States. Unemployment is at a record high but the Dow Jones keeps rallying up. At some point, property prices will be next. In Australia, the record low-interest rates will remain until employment figures improve.

So in my opinion (in the short term), property prices may have a bit more room to drop due to COVID-19’s impacts on the economy, in addition to the confidence and market perception of buyers. Again this is just my thoughts and opinions. However, once we develop a vaccine and gain some normality again – property as an asset class is likely to continue to perform relatively well in the long run.

The bottom line

Buy when you can afford to, not based on what the media is telling you and hold out for a long-term view.